TRANSCRIPT – edited for clarity

INTRO: Hi friends, this is Suri Stahel. Thanks for taking some time to join me again on Doing Things on Purpose – the podcast that empowers women to take charge of their time, health, relationships, and money by doing things on purpose.

MOM CHECK-IN: In today’s mom check-in, I invite you to just stop whatever it is that you’re doing right now, if possible.

Slowing down with the breath

Let’s spend a few minutes just breathing, to calm the mind together. We’re going to practice boxed breathing, which everyone from yogis to the navy seals use to quickly balance the nervous system :

- We’re going to breathe in to the count of 4.

- Hold for 4.

- Breathe out for 4.

- Hold for 4.

- Then we’ll repeat this sequence twice more.

Let’s begin…

Breathe in, 2, 3, 4. Hold, 2, 3, 4. Breath out, 2, 3, 4. And hold, 2, 3, 4. (repeat 3x)

Now let your breath return to it’s natural rhythm, and see how you feel. There are many other breathing variations you can try:

- I quite like the 4-4-6-2 sequence where you exhale longer than you inhale.

- Or you can also try the 4 in, 7 hold, and 8 out sequence.

What this does, is to balance or calm our nervous system:

- Breathing in naturally increases your hear rate – stimulating your sympathetic, fight and flight system.

- While breathing out slows your hear rate – activating your parasympathetic, rest and relax system.

- We need both of these systems to work in balance with each other.

Know that you can always return to the breath in this way, whenever you feel stressed or overwhelmed. It doesn’t always work completely, but it always helps.

When kids ask: When can we afford a house?

Moving on to today’s episode titled: When can we afford a house? This week, I wanted to give you a quick peek into what happened in our household last week, to prompt this discussion.

As you might now, I have two girls aged 9 and 11. They play a lot with each other and they’ve been dreaming about buying a house and living together when they grow up – so they can have all the things that little and big girls dream of such as pets and a big garden, where they can live happily ever after.

So last week, they asked me:

Mommy, if we put together the money that daddy saves in our account each month – when can we afford to buy a house?

I loved this question, because of course kids really have no idea how much a house even costs these days. Many adults don’t either.

How much does a house cost?

From my quick google search, as of early 2024:

- The average home price in Switzerland where we live, averages $1.2 million (USD).

- In the US, the average is around $400,000.

- And In Malaysia, where I was born, it’s about $95,000 (or MYR 450,000).

Of course we all know that if you want a comfortably-sized home in a good location, that price is going to perhaps double or even triple.

But let’s just work with these average prices for now.

How much have we saved so far?

So to answer my kids’ question, let’s find out: How much do they even have?

We’ve been saving USD 110 (or CHF 100 ) combined, for our kids per month, since birth. I would love for this number to move up to CHF 200 or even CHF 400 per month combined, but it’s just not the case for us right now.

- Before learning how to invest, we saved their money the way most parents do – in a youth savings account (with ZKB) returning around 1% annually – which in Switzerland, is considered high. In this account, they now have a combined amount of around $14,500 (USD). I’m as amazed as you – how even the small amounts that we set aside, has added up over time.

- After learning to invest since one and a half years ago, we’ve saved about $2,000 (USD) for them in a brokerage account, which we manage. Currently, it’s returned 37% in the past one year. So from the original $2,000 savings, their investments are currently valued at around $2,700.

I’m quoting everything in US Dollars to keep things simple.

A 30-Year Investment Horizon

Assuming my kids would want to buy a house by the time they’re 40. They’ll have around 30 years to save and invest for it.

So let’s calculate how much they’ll have in 30 years.

Here’s what I did:

- Google, and open NerdWallet’s Compound Interest Calculator.

- Look at their Youth Savings Account – assuming we keep it there:

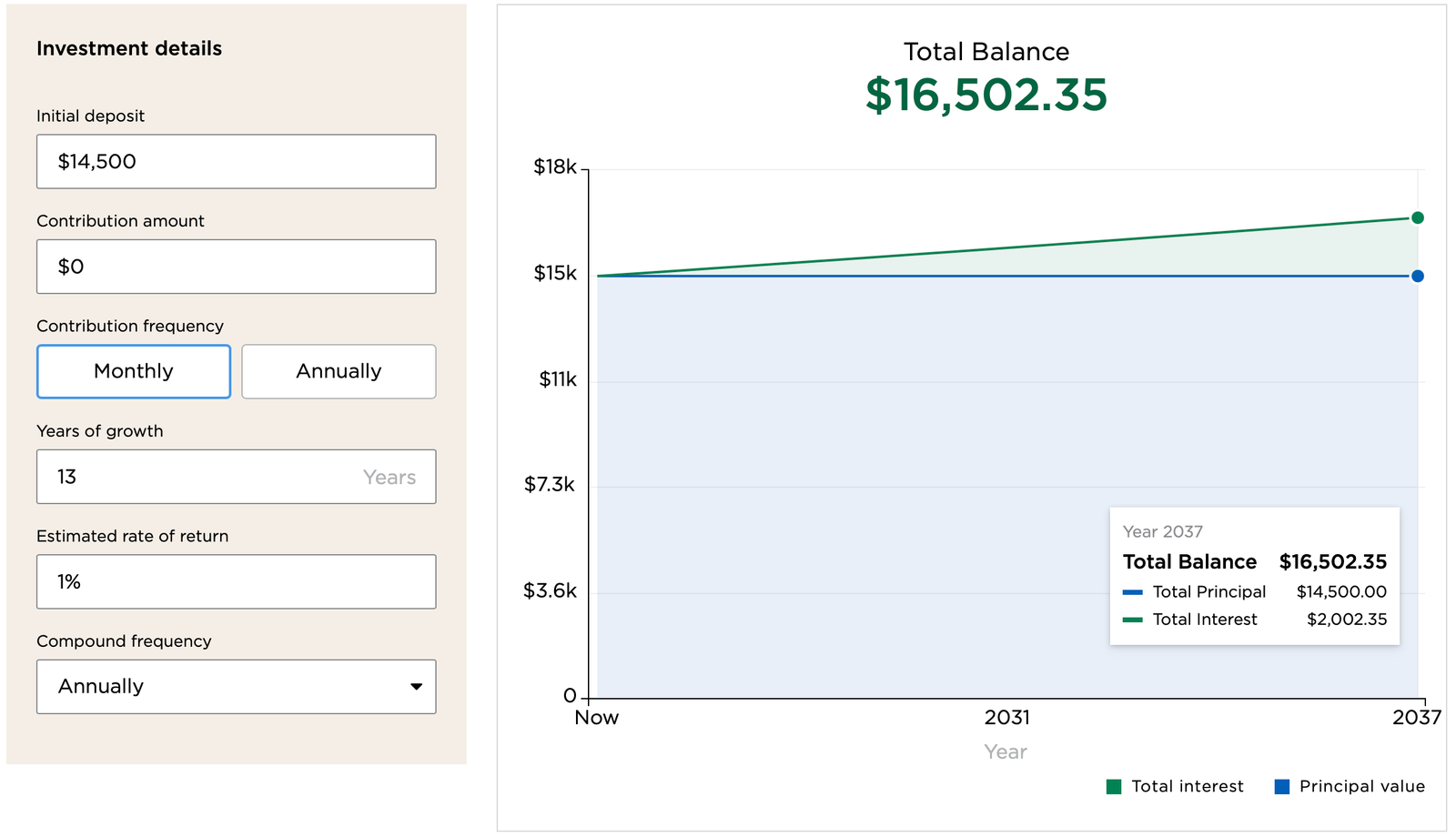

- Their current balance is $14,500. Let’s type this in as the “initial deposit” in NerdWallet’s calculator.

- We’re no longer funding this account so the “contribution” amount will be zero.

- “Years of growth” will be 13 for simplicity’s sake, until our eldest reaches 22, which is the age limit for this type of account.

- Let’s assume the “return” will stay at 1% per annum.

- So in 13 years, when the money is taken out, it will have grown to $16,500 – that’s a gain of just $2,000 or a ROI of 13%.

- What happens to this money after we take it out?

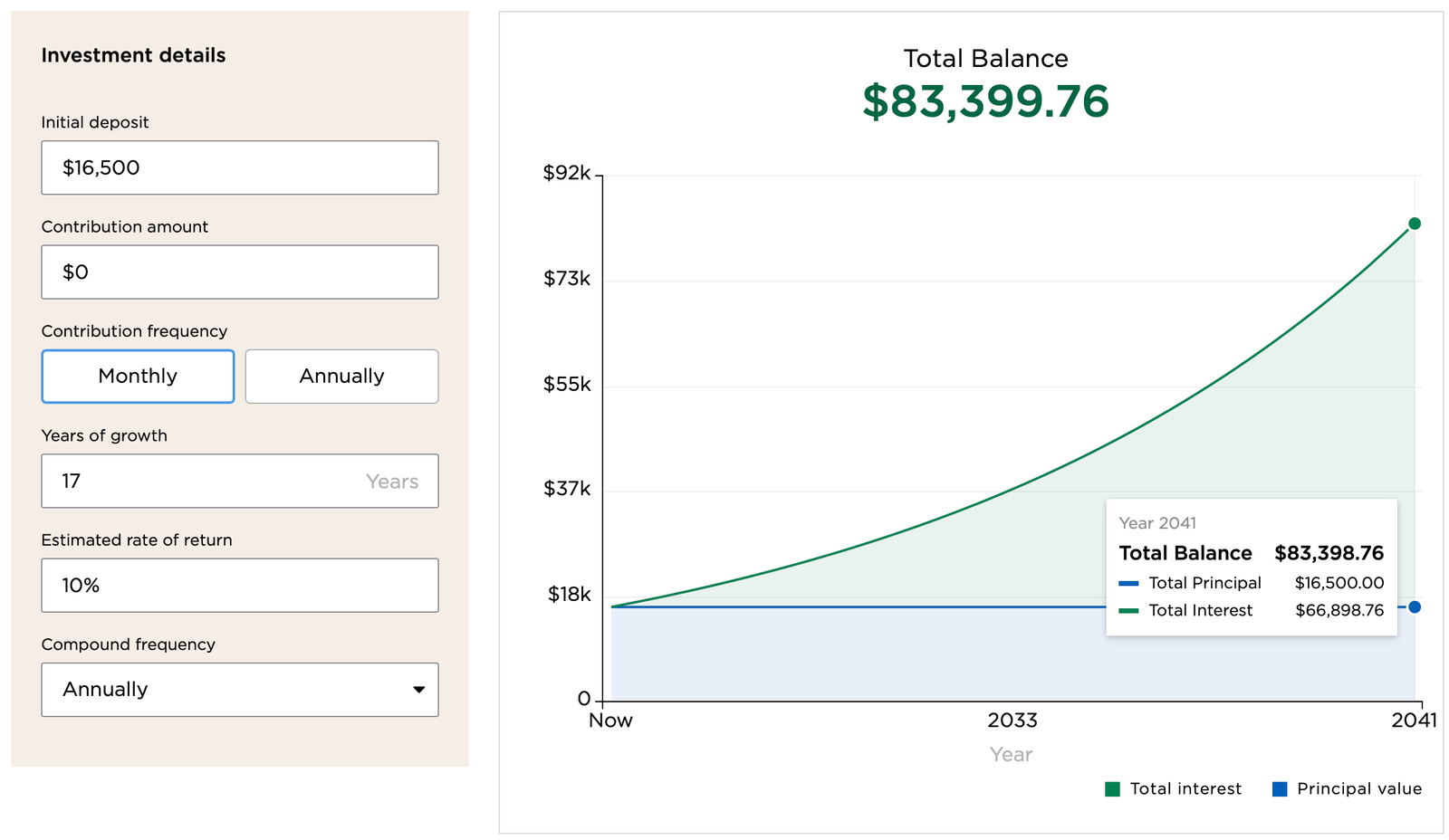

- For the rest of the 17 years until they reach 40, let’s assume we deposit this money into their private brokerage account.

- So we input $16,500 back into the calculator.

- Let’s assume the market returns 10% annually, which is the historical average rate of return for an index fund or ETF tracking the world market like VT or VWRL, and reinvest all dividends.

- We put zero contributions in, and let it run for the remaining 17 years.

- By the time the girls turn 40, this amount will have grown to $83,400 – that’s the original $16,500 in principal, plus $66,900 in compound interest gained, or 405% return on investment.

- Secondly, we look at their self- (or currently parent-) managed brokerage account:

- It has a current value of $2,700 (USD). Let’s input this value in the calculator.

- We add a $110 contribution per month into it, which is what we’re currently able to save for the girls (CHF 100 to be exact).

- Let that also run at a modest 10% annual return for the next 30 years.

- In 30 years, this account will return $274,000 by the time my girls reach 40 – that’s $42,300 in principal, plus $231,700 in interest gained, or a 548% ROI.

The result?

Combined, their invested savings will have returned approximately $357,000 in 30 years, before my kids reach 40.

Of course, there can be many more variables to consider:

- Firstly, if their current brokerage portfolio continues to return 37% as it currently did in the past year – even if we never put any new money in, their investment portfolio would grow from $2,700 to a whopping $34 million in 30 years. 🤯 That’s mind blowing AND it’s wishful thinking. Since the markets do need go up and down to remain healthy – albeit with a general upward trend.

- On the other hand, what if the markets only end up averaging 7% annually instead of 10%? If all else remains as initially calculated, my girls would only end up with $201,000 instead of $357,000 to buy their house in 30 years time.

- Thirdly, another assumption could be that after 15 years, when the girls turn around 25, they’re already working and can perhaps fund their investments above the current amount that mom and dad are saving for them. Maybe even up to $1,800 per month, combined? That’s quite a lot, but that would allow them to even reach $1,000,000 by the time they’re 40.

- Lastly, and probably the biggest variable and contributer to wealth growth – is if we as parents are able to contribute even a little more for our kids TODAY. Even if you start with zero now, a $200 monthly investment would amount to $412,500 in 30 years, at the average 10% annual rate of return. That’s even more than what we’ve just calculated for our girls, despite their existing initial savings, but at our lower $110 per month savings rate.

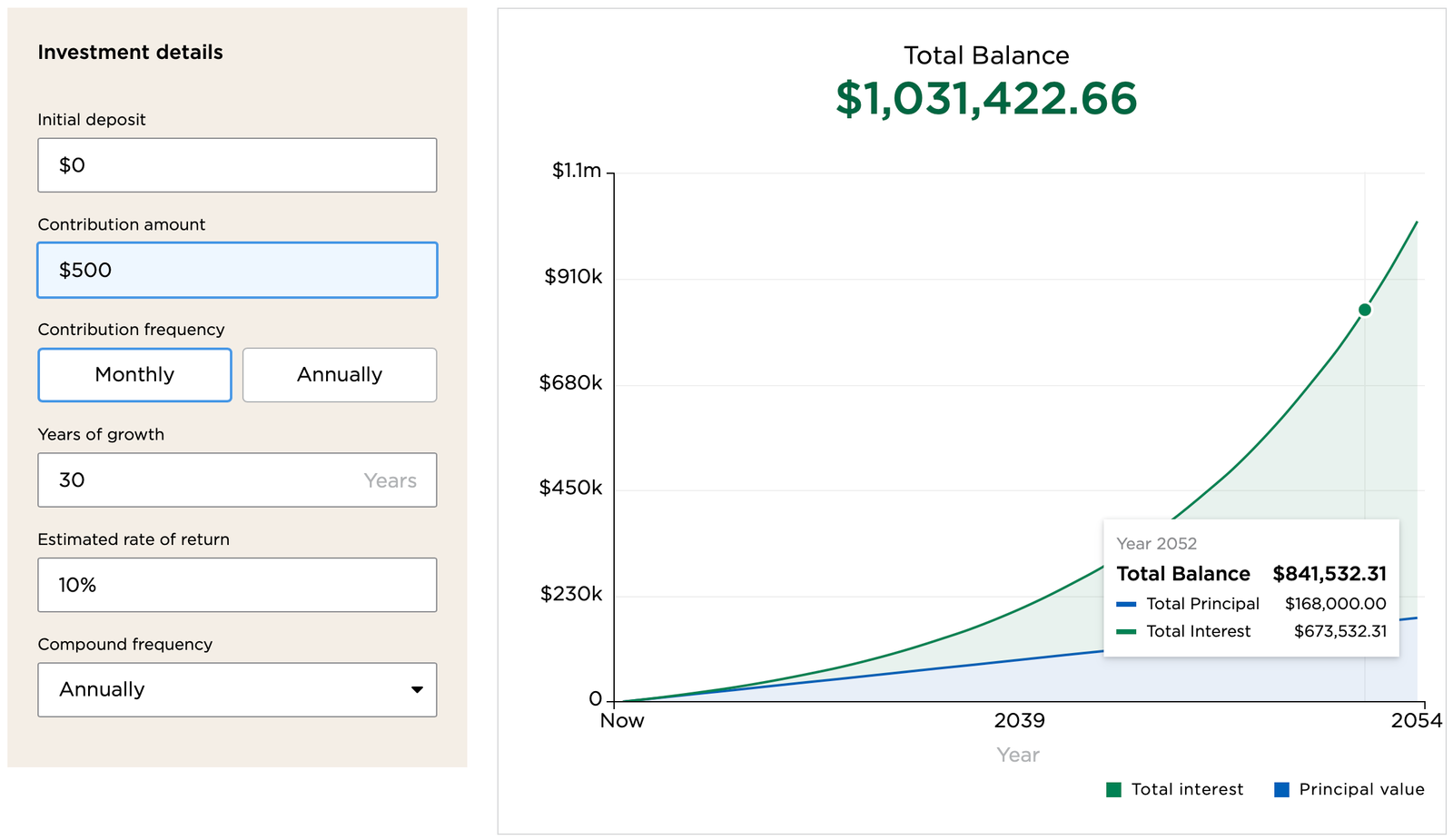

And the magic number? If you can invest $500 per month for your kids from today, it can return $1,000,000 in 30 years (again with the 10% average rate of annual return).

Of course nothing is ever guaranteed. Would we even want to help our kids be millionaires by 40, without any effort of their own? Probably not.

Nobody wants to spoil their kids… But I think, it’s just a nice-to-know number. And something to perhaps, motivate many of us to start investing, if we haven’t already.

The golden rules of investment

Never forget the two rules of investment:

✨ The best time to invest was yesterday, the second best time is today – I agree, but it helps to time your entry a little bit, when the markets are slightly down (but set a deadline).

✨ Start investing as much as you can, as early as you can – Because the longer you stay invested – the higher your compounded rate of return, and the lower your risk of loss.

So maybe your parents, like mine, never taught you about investing. Understandably it’s a little tough to play catch-up.

💰 To both save and invest for your kids, as well as for yourself and your spouse, for your old age.

Just do your very best right now

Let’s give ourselves time to slowly break this generational cycle of money illiteracy. To start good money habits today, that we happily can pass down to our children tomorrow, and their children.

When can my kids afford a house?

Assuming they pay fully by cash:

With $357,000? Maybe not in 30 years… Unless they decide to settle down in a more affordable country compared to Switzerland. Or if they earn enough to save more than we ever could for them each month.

But in 40 years? Probably. If they maintain our current savings rate of $110 per month for them, which would make them reach a million by the time they’re 50.

So really – it’s up to them. As it should be. But we’ve certainly helped them start off, on the right foot and that all we can do.

What about you? If you haven’t already, I wholeheartedly encourage you to play with the NerdWallet calculator to see how your savings and investments can grow over time.

Again, I’ll link to the calculator I used on the show notes at suristahel.com/22.

Need more help?

- Read my comprehensive guide on money and investing at: suristahel.com/money

- Or click on the category “money” under the podcast section of my website.

- You can also follow me on Twitter, Facebook or Instagram for short tips on money, and managing life with a family.

- Send your questions at: suristahel@gmail.com

That’s all I have for you today. I hope this has been helpful.

Thanks again for listening to Doing Things on Purpose, with me Suri. I’ll catch you again next time.